The Employment Insurance Operating Account was created on 1 January 2009. It is a consolidated specific purpose account, meaning that it includes program-related revenues credited and expenses charged to this account under the Employment Insurance Act.8 EI premiums are paid into the Consolidated Revenue Fund (CRF), which includes general government revenues such as taxes,9 and the benefits are paid out of it.10 Each year, all EI program expenditures are charged to the CRF and all program-related revenues are credited to it. The results are published in the Public Accounts of Canada. The Account’s annual deficit or surplus is included in the federal government’s financial statements.

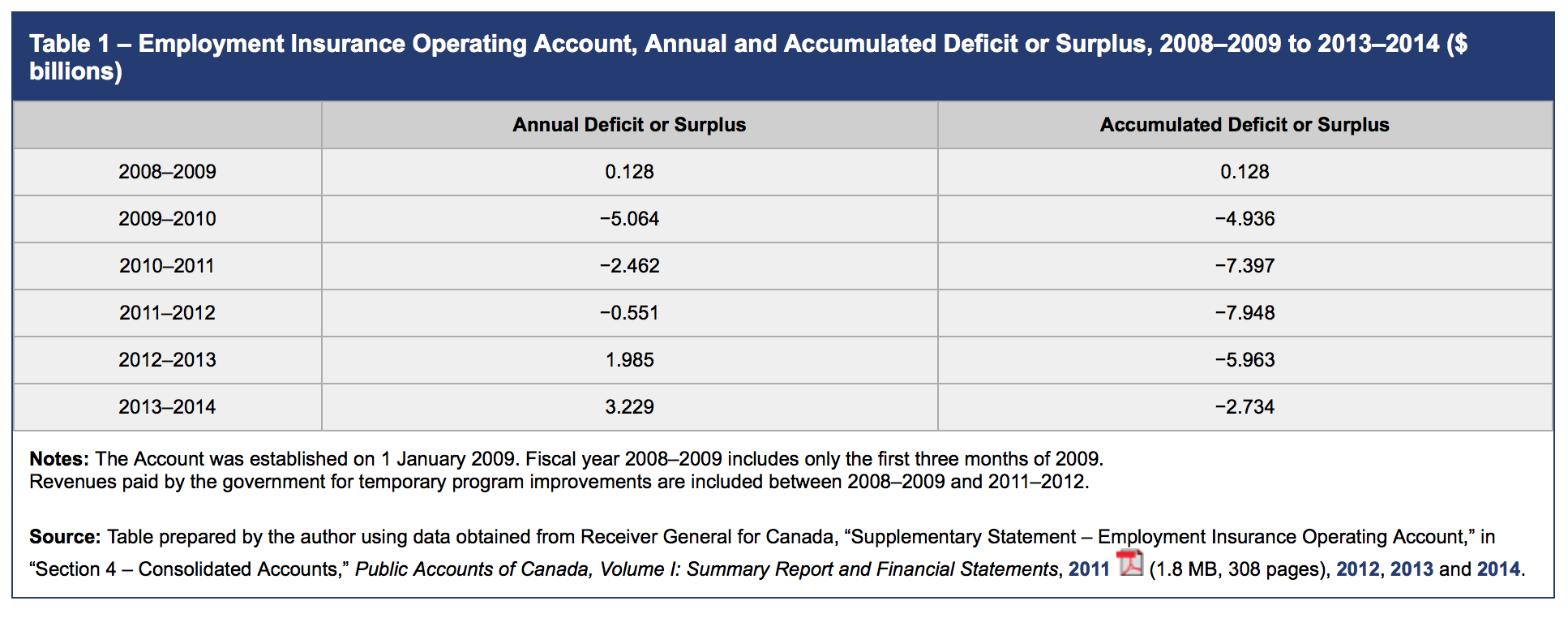

As of 31 March 2014, the Account had an accumulated deficit of $2.7 billion. For 2013–2014 alone, the Account had a surplus of $2 billion.11

Table 1 – Employment Insurance Operating Account, Annual and Accumulated Deficit or Surplus, 2008–2009 to 2013–2014 ($ billions)

Chosen excerpts by Job Market Monitor. Read the whole story at Employment Insurance Financing.

Discussion

Trackbacks/Pingbacks

Pingback: Canada – L’assurance-emploi doit se recentrer sur le remplacement du revenu des personnes ayant perdu leur emploi selon un rapport de l’IRPP | Job Market Monitor - July 24, 2015

Pingback: Employment Insurance in Canada – Five key changes | Job Market Monitor - April 21, 2016