Bernanke : While I do not see much evidence of any significant increase in structural unemployment so far, I am concerned that structural unemployment could increase over time if the labor market heals too slowly–a phenomenon known as hysteresis.

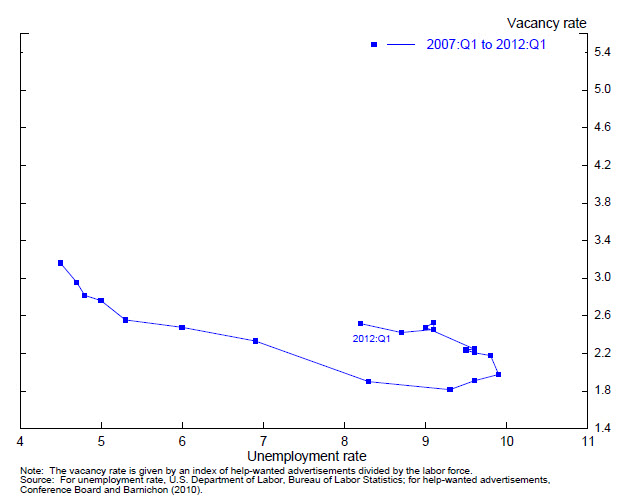

I do not interpret data suggesting an outward shift in the Beveridge curve as providing much evidence in favor of an increase in structural unemployment. The Beveridge curve plots the relationship between unemployment and job vacancies. Cyclical variations in aggregate demand tend to move unemployment and job vacancies in opposite directions, whereas structural shifts would be expected to move vacancies and unemployment in the same direction. For instance, a structural mismatch between businesses’ hiring needs and the skills of unemployed workers would tend to push up the level of vacancies for a given level of unemployment. Figure 3 plots the co-movement of unemployment and job vacancy rates since 2007.5 Consistent with a substantial decline in aggregate demand, followed by some modest recovery, movements in unemployment and vacancies since 2007 display a predominantly inverse relationship. However, figure 3 shows that as job vacancies have risen during the recovery, unemployment has declined by less than might have been expected based on the relationship that prevailed during the contraction. This outcome has led some to suggest that the Beveridge curve has shifted outward, reflecting an increase in the extent of job mismatch. In my view, a portion of this apparent outward shift in the Beveridge curve reflects increases in the maximum duration of unemployment benefits, which have been important in buffering the effects of the weak labor market on workers and their families. The influence of these benefits will dissipate as they are phased out and the economy recovers. In addition, loop-like movements around the Beveridge curve are common during recoveries. Vacancies typically adjust more quickly than unemployment to changes in labor demand, causing counterclockwise movements in vacancy-unemployment space that can look like shifts in the Beveridge curve. Figure 4 plots the relationship seen during and after the 1973 and 1982 recessions alongside the current episode. As can be seen, such counterclockwise movements also occurred during these two earlier deep recessions.

Figure 3

Figure 4

While I do not see much evidence of any significant increase in structural unemployment so far, I am concerned that structural unemployment could increase over time if the labor market heals too slowly–a phenomenon known as hysteresis. An exceptionally large fraction of those now unemployed–more than 40 percent–have been out of work for six months or more. My concern is that individuals with such long unemployment spells could become less employable as their skills deteriorate and as they lose their connections to the labor market. This outcome does not appear to have occurred in the wake of previous U.S. recessions, but the fraction of the unemployed who have been out of work for a long period is much higher now than it has been in the past. To date, I have not seen evidence that hysteresis is occurring to any substantial degree. For example, the probability of finding a new job has not deteriorated more for individuals experiencing a long-term bout of unemployment relative to those facing shorter spells. Nonetheless, the risk that continued high unemployment could eventually lead to more-persistent structural problems underscores the case for maintaining a highly accommodative stance of monetary policy.

Putting all the evidence together, I see no good reason to doubt that our nation’s high unemployment rate indicates a substantial degree of slack in the labor market. Moreover, while I recognize the significant uncertainty surrounding such forecasts, I anticipate that growth in real gross domestic product (GDP) will be sufficient to lower unemployment only gradually from this point forward, in part because substantial headwinds continue to restrain the recovery…

Source:

Read More @ FRB: Speech with Slideshow–Yellen, The Economic Outlook and Monetary Policy–April 11, 2012.

Discussion

Trackbacks/Pingbacks

Pingback: China | Skill Gap | A structural problem « Global Job Gap, Local Skills Gap - April 16, 2012

Pingback: Long-Term Unemployment is not a short term problem « Global Job Gap, Local Skills Gap - May 7, 2012

Pingback: The overlapping structural problems « Global Job Gap, Local Skills Gap - May 9, 2012

Pingback: It’s not a skill mismatch: Disaggregate evidence on the US unemployment-vacancy relationship | vox « Job Market Monitor - January 5, 2013

Pingback: US / It is a Long-Term Unemployment Crisis « Job Market Monitor - February 15, 2013

Pingback: US / The Beveridge Curve is shifting | Job Market Monitor - March 8, 2013