The unemployment insurance (UI) system has played an important role in delivering relief during the current pandemic. At the same time, this experience has highlighted the important challenges facing the UI system due to poor and underfunded administrative capacities, too few unemployed workers qualifying for UI benefits, inadequate levels of regular UI benefits, lack of effective triggers to tie benefit duration to economic conditions, and meager utilization of work sharing programs. In this proposal, I suggest remedies for each of these problems, and argue that these remedies are best achieved through converting the UI system to a fully federal program.

In light of past evidence on the costs and benefits of the UI system, and to address some of the key existing shortcomings in the current UI system, I propose five key changes, which I discuss in detail here.

Proposal 1: Make UI A Federally Financed and Administered Program

Under my proposal, UI will be made a fully federally administered program, like Social Security. Part of the costs of the program—reflecting regular benefits paid during normal times—would be paid using a federal payroll tax, while the balance would be paid using general federal revenue. I recommend that the payroll tax be levied on both employers and employees, similar to Social Security. Since the current system is based only on employer taxes, there will be some added costs on workers. However, note that even when employers nominally pay a payroll tax, it is partly paid for by workers through lower wages. In other words, if all of the added taxes needed to pay for the proposed benefits were nominally on employers, some of those taxes would be passed through to workers as lower wages. At the same time, the pass-through of employer taxes to wages is likely to be incomplete, which is why employers often lobby against increases in the tax rates. Importantly, as O’Leary and Wandner (2018) argue, moving away from an employer-only system could reduce some employer opposition to changes in benefit generosity.

Under my proposal, the payroll taxes would be set to pay for expenses during normal times, not downturns, and should be within a range that does not vary by the business cycle. (The range allows for some degree of experience rating, whereby taxes depend on the extent of use of benefits among workers laid off by a particular firm.) To be specific, the payroll tax rate schedules should be set to allow revenues to equal to outlays for benefits under Tiers 1 and 2 of benefit durations, as described in Proposal 2 below; in brief this means funding up to 33 weeks of UI spells. All of the cyclical financing should come from general funds. The lack of cyclical changes in tax rate schedule can help in the economic recoveries. In addition, the use of general funds from the federal budget to pay for cyclical UI helps provide greater stimulus during economic recoveries. Moreover, this automatically increases revenue collection during extended booms (without any pressure to cut the rates), thereby stabilizing activity.

Finally, the federal government should use all available earnings sources from UI employment and earnings data (ES-202 filings by employers) to automatically calculate the benefit levels. (The formula the federal government would use to automatically calculate those levels is described in Proposal 4.) Employers should also be required to report workers’ hours and not only earnings as they do currently in four states. When they file for UI, applicants should automatically be shown the default benefit level based on their earnings records on file.

Proposal 2: Expand Eligibility

In order to increase recipiency, I make the following recommendations.

Reduce the earnings eligibility threshold, setting the minimum earnings requirement at $1,000 in one quarter and $500 in a second quarter during the base period, allowing for both standard and alternative base periods. These thresholds are substantially lower than those used in most states. Having a more-realistic and more-consistent earnings eligibility threshold can go a long way toward raising eligibility. Both reducing the earnings thresholds and allowing for the alternative base period increase the odds that an unemployed worker qualifies for UI. These thresholds should be indexed to the median average weekly wage (AWW), similar to suggestions made by O’Leary and Wandner (2018).

Allow good cause voluntarily separating workers to be eligible for UI. This allowance would include workers who may see change in work circumstances (such as wage or hour cuts) that are beyond the worker’s control; and workers who have to quit due to extenuating family circumstances, such as own or family-member health reasons, or when child-care arrangements cannot be secured, or when a spouse or partner relocates. This recommendation is similar to suggestions in West et al. (2016) and Bennet (2020). Moreover, most of these conditions are covered by provisions that are already in place in at least some states, but under my proposal these provisions would be applied uniformly across the country.

In order to raise awareness and reduce the cost of application, the federal government should automatically send a letter to employees about potential eligibility when they separate from an employer.

Finally, the federal government should implement a Jobseeker’s Allowance (JA) program for those who are unemployed and searching for work, but who do not qualify for regular UI, closely following the proposal in West et al., 2016. This group would include those who are self-employed, those with inadequate earnings history, new entrants, and reentrants to the labor market.

A key requirement would be that these individuals are actively seeking employment; to mitigate abuse the work search requirements should be more stringent for this group of workers than for regular UI recipients. Another way to mitigate concerns of abuse of the program is through making the assistance substantially less generous than regular UI, and by imposing a time limit of receipt (see West et al. 2016 for a detailed presentation of a JA plan). Under my proposal, the JA benefit level would be set at 20 percent of the AWW. The JA PBD in ordinary times would be 13 weeks (or half of usual length of regular UI benefits). The JA PBD would also respond to the same state and national triggers that would determine the regular UI PBD, as discussed in Proposal 3 below. In particular, the JA PBD should be set at UI PBD less 13 weeks. However, there would be additional limits on collecting the JA, with a 52-week total limit in any rolling five-year period. The JA program would be funded entirely out of regular federal funds.

Overall, how will these reforms affect recipiency rates? While it is difficult to answer this precisely, I estimate that combination of reforms could lead to a recipiency rate among the unemployed of around 55 percent, which was double the recipiency rate in 2019 nationally. For reference, in 2019 the three states with the highest recipiency were New Jersey (59 percent), Massachusetts (50 percent), and Connecticut (47 percent), averaging at 52 percent. I am assuming that the combination of reform will push the national recipiency rate to the current frontier across states. While it is difficult to project take-up of a new program, I estimate that JA would cover an additional 10 percent of the unemployed, based on the use of PUA during the pandemic.

Proposal 3: Tie potential benefit duration (PBD) to State and National Triggers

The key recommendation is to reform the current EB program to accomplish three objectives: (1) remove the look-back period, (2) add more tiers to allow for adequate increases in the PBD during downturns, and (3) include both national and state triggers to allow for a robust response at the national level while allowing for heterogeneity across local areas. Since the IUR triggers have largely been irrelevant for EB triggers, following Chodorow-Reich and Coglianese (2019) I recommend focusing on TUR triggers.

In particular, I recommend seven tiers of PBD for the proposed federal UI program, where the PBD will depend on the maximum of state or national triggers for total unemployment rates (TUR):

Tier 1: Under 5 percent (26 weeks)

Tier 2: 5 percent (33 weeks)

Tier 3: 6 percent (46 weeks)

Tier 4: 7 percent (59 weeks)

Tier 5: 8 percent 72 weeks)

Tier 6: 9 percent (85 weeks)

Tier 7: 10 percent (98 weeks)

To be concrete, if someone is in a state with a 10 percent unemployment rate while the national unemployment rate is 7 percent or higher, they would be in Tier 7 (with a PBD of 98 weeks). Similarly, if someone is in a state with 7 percent unemployment rate while the national rate is 10 percent, they would also be in Tier 7. What is the rationale for a national-level trigger beyond just a state-level one? If there is a clear signal that we are entering a national recession, it is useful to provide broad-based support and not wait until a particular state has officially crossed a threshold. State and national unemployment are both imperfect proxies for local labor market conditions, but state-level estimates are noisier signals, especially for smaller states. For this reason, if we see national level unemployment rate climb above 5 or 7 percent, it provides important information about the likely trajectories of the local labor market.

If the proposed triggers were in place, what would the PBD have looked like in the United States over the past two decades? To answer this, I simulate state-specific PBD based on state and national triggers. Figure 1 plots the average PBD across the United State over time, along with the national unemployment rate.

As figure 1 shows, during the extended Great Recession period (2008–12), the proposed policy would have raised the (average) PBD to levels that are broadly similar to what was discretionarily achieved via Emergency Unemployment Compensation over that period. For example, in 2011 the average PBD across states was 87 weeks, while under my proposal it would have been 85 weeks. Seventeen states would have had greater PBDs and 34 states would have had lower PBDs under my plan. At the same time, under my proposal the PBD would have increased more quickly during the Great Recession, making it a better automatic stabilizer. Under the proposed rules, the average PBD would have increased from around 30 weeks to 85 weeks between 2007 and 2009. In contrast, the PBD in reality increased from 26 to 68 weeks between those periods, and it took until 2011 for the PBD to catch up to my proposed rule. Another benefit is that by using triggers the phasing out of extended PBD would be smoother. For example, the Emergency Unemployment Compensation expired in 2014 rather abruptly, leading PBD to fall from as much as 99 weeks to 26 weeks in some states. In contrast, under my proposal PBD would have fallen more gradually based on both national- and state-level unemployment rates, falling to around 40 weeks by 2015 and to 26 weeks by 2017 when the labor market was considerably tighter.

Finally, in 2019—a year with a tight labor market—the average PBD was around 25 weeks while under my plan it would have been 27. In general, my proposed triggers would match the severity of the crises. For example, in the aftermath of the shallower 2001 recession, average PBD would have risen to a little under 50 weeks for a brief period, and stayed mostly under 40 weeks during the recovery period. In contrast, during the onset of the current crisis, PBD would have shot up to 98 weeks, but fallen as the labor market improved. However, it would have been close to 60 weeks in February 2021, which is broadly similar to where we were in actuality (average of 58 weeks).

Overall, while the proposed changes would alter the distribution of PBDs across place and time (to better match economic necessity), it would only modestly increase the overall number of weeks. The average PBD in the 2015–19 period would have been 30 weeks under my proposal, while in reality it was 25 weeks. During the 2010–14 period, the average PBD would have been 71 weeks under my proposal, as compared to 62 weeks in reality.

Proposal 4: Restructure and Increase the Benefit Replacement Rate

I propose the following benefit replacement determination. Regular UI benefits would be based on the AWW as follows (assuming that maximum and minimum benefits do not bind):

First $400 of AWW: 80 percent marginal replacement rate

Next $300 of AWW: 65 percent marginal replacement rate

For additional AWW above $700: 50 percent marginal replacement rate

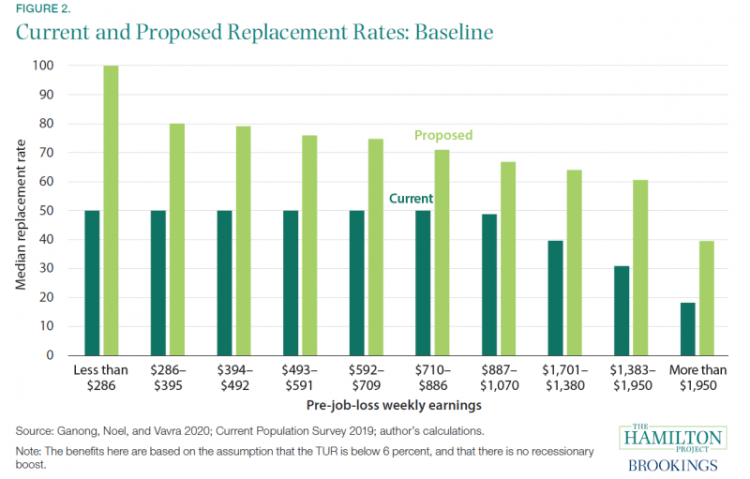

I propose setting the maximum benefit level at 80 percent of AWW, and a minimum benefit level at 20 percent of AWW in the United States. For example, in 2020 this would have meant a maximum benefit of $910 and a minimum benefit of $230. This is close to what states with more-generous benefits currently do; for example, in Washington State the minimum benefit level is $201 while the maximum benefit is $844. In addition, replacement rates would be capped at 100 percent of earnings for all workers. The benefits would be calculated based on the high-quarter method, as is done in 29 states currently, which protects workers with nonstandard and limited work histories. Specifically, this proposed change would take the highest quarter in the relevant base period for the purpose of benefit calculations. To show how the current and proposed replacement rates look for different workers, figure 2 shows the average replacement rates by earnings deciles of those who are unemployed. These data are based on pre-pandemic 2019 unemployed workforce in the Current Population Survey (CPS), based on the methodology developed in GNV. More details are provided in appendix A.

As we can see, the average replacement rate for those in lower deciles is around 70–75 percent, declining to 40 percent at the top decile. In contrast, the current replacement rates (averaged across states) are around 50 percent for the bottom two-thirds of the workforce, declining to around 20 percent at the top. Moreover, the averages in the current replacement rates mask considerable heterogeneity by state. In contrast, under my proposal replacement rates would not vary by state for workers with the same earnings levels. Based on the simulations, the average weekly benefit levels in 2019 would have risen from $338 to $547 under my proposal, leading to an average replacement rate of 72 percent (as compared to the estimated current replacement rate of 44 percent).

In addition, I propose a boost to benefit levels during downturns to aid the automatic stabilizer role of UI policy, and because it is less costly (in terms of efficiency losses) to provide more-generous benefits during downturns. In particular, the recessionary boost would entail

An additional $100/week boost above 6 percent national TUR; and

An additional $200/week boost above 8 percent national TUR.

Figure 3 shows the same distribution, but now with a recessionary boost of $100/week. Here we see higher replacement rates throughout the distribution. A substantial portion of the beneficiaries in the bottom half of the distribution would be at the 100 percent replacement cap during downturns. The beneficial stimulus effects and the reduced cost of moral hazard (due to search externalities) allows a moregenerous benefit level during downturns.

To estimate the resulting increase in outlays on UI benefits, I simulate the stimulus spending that would have occurred had the recessionary boosts been in place since 2000. To clarify, these are just the added spending from the recessionary boost assuming the recipiency rates in this proposal; I will provide estimates for the overall added spending—including the change in regular benefit levels and recipiency rates—in the subsection on proposal costs below. In addition, note that the estimates for 2020 do not account for payments from FPUC. Figure 4 plots the simulated annual federal spending from the recessionary boost over this period.

Here are the key findings: During the extended Great Recession period (2008–14), the proposed recessionary boost would have provided an additional $320 billion or so in added stimulus—or roughly $45 billion per year. The proposed recessionary boost is proportionate to the size of the downturn: for example, it would have added a smaller boost of around $35 billion during the 2001 recession. Finally, during the current crisis, the automatic recessionary boost would have provided around $40 billion in added spending in 2020. In comparison, policymakers spent around $250 billion toward the boost in benefits in 2020. However, this comparison does not factor in the added spending that occurs under my plan from more generous baseline benefits. Factoring those in, as I do in the proposal costs subsection below, suggests a total of around $150 billion in added expenditures in 2020 from the proposed increase in benefit levels as compared to normal replacement rates (i.e., excluding FPUC or LWA).

It is also useful to keep in mind how UI income interacts with other safety-net programs to affect income after taxes and transfers. In particular, the Supplemental Nutrition Assistance Program (SNAP) is an important program that has important countercyclical properties. There is a strong distributional argument to exclude the UI recessionary boosts for the purpose of SNAP eligibility determinations in order to help those at the very bottom, to avoid SNAP eligibility reduction to crowd out the recessionary boost. Such an exclusion was adopted as part of the December 2020 relief bill, but only temporarily. Under my proposal the UI recessionary boost income would be excluded for SNAP eligibility determination at all times.

Proposal 5: Strengthen Short-time compensation (STC; also called work sharing)

Incorporate STC into UI at the federal level, and substantially increase administrative capacity and funding to process applications in a timely fashion. Streamline the employer application process by allowing online applications, using data from the regular employment and wage (ES-202) employer filings as a default, allowing employers to choose from the list of existing workers who they wish to enroll in STC. Information about hours should already be collected as part of the regular employer filings, making this process easier. Moreover, similar to what was suggested by von Wachter (2020), the federal government should allow employers to pay workers on STC directly, and should compensate employers for the cost through the STC program.

Increase awareness about the program through a major information

campaign using strategies that have been found to work (as in Houseman et al. 2017), and test the efficacy of other messaging campaigns. This echoes the proposal made by Abraham and Houseman (2014).

Allow employers to reduce hours by as much as 80 percent of enrolled workers, which will allow greater employer participation. This was proposed by then-candidate Biden in his 2020 position statement (Biden Harris 2020).

Provide financial incentives to employers to use STC by providing a refundable tax credit to reimburse employers for the added costs of providing full health benefits for workers during the period of reduced work hours. This also was proposed in the Biden position statement (Biden Harris 2020).

Source: A Plan to Reform the Unemployment Insurance System in the United States | The Hamilton Project

Discussion

No comments yet.