The CIA is proposing changes to the age at which benefits should be made  available to Canadians under Canada’s retirement income systems and tax-assisted private savings programs, specifically the Canada Pension Plan/Quebec Pension Plan (CPP/QPP), Old Age Security (OAS), and registered pension plans and Registered Retirement Savings Plans (RRSPs).

available to Canadians under Canada’s retirement income systems and tax-assisted private savings programs, specifically the Canada Pension Plan/Quebec Pension Plan (CPP/QPP), Old Age Security (OAS), and registered pension plans and Registered Retirement Savings Plans (RRSPs).

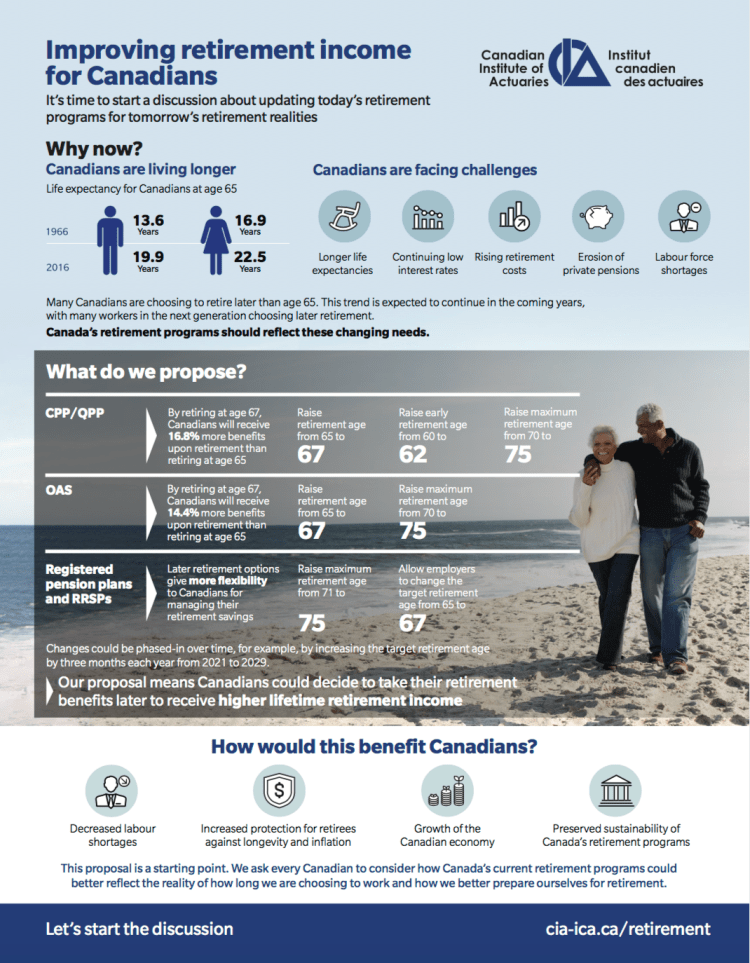

This document is intended to engage all Canadians in a healthy and much-needed discussion of changing societal needs and the best retirement program designs to support those needs.

Our proposal serves as a signal to Canadian workers as they plan for retirement, and will help those workers who have not yet prepared and saved adequately for retirement to make realistic decisions.

The CIA wants to highlight that the CPP/QPP and OAS/Guaranteed Income Supplement (GIS) as they are designed today are projected to be financially sustainable for the next 40 to 75 years, and that these plans provide the best available protection against the combined risks of inflation and longevity to Canadians with no other retirement income.

The proposed changes are designed to alter the timing of when benefits are collected by Canadians and will preserve the financial sustainability of these programs.

We propose the following to legislators:

CPP/QPP

a. Defer the target eligibility age from 65 to 67 with a commensurate increase in the target retirement benefit

of 16.8 percent. This proposal does not change the amount of CPP/QPP to be received at age 65 or at age 67.

b. Defer the minimum early retirement age for the CPP/QPP from 60 to 62.

c. Defer the maximum postponed retirement age from 70 to 75.

OAS

a. Defer the eligibility age from 65 to 67 with a commensurate increase in the target benefit payable of 14.4 percent.

This proposal does not change the amount of OAS to be received at age 67.

b. Defer the maximum postponed retirement age from 70 to 75.

Registered pension plans and RRSPs

a. Provide greater exibility for individuals to manage retirement income by deferring the maximum age for commencing receipt of income from 71 to 75.

b. Allow employers to change the target retirement age

in registered pension plans from 65 to 67 on a go-forward basis, with any accrued bene ts being subject to a commensurate adjustment. This proposal does not change the amount of pension for accrued benefits under private plans.

In addition, the CIA also proposes that governments consider the following actions:

1. Establish an automatic review period for the age of eligibility for full benefits, such as five or 10 years, to consider future adjustments based on changes in the life expectancy and needs of Canadians.

2. Continue to undertake a regular review of the early and postponed retirement adjustment factors of CPP/QPP and OAS to ensure that they do not encourage early retirement or discourage deferred retirement.

3. With respect to the GIS, the government should revise existing GIS clawback provisions with the intent of providing incentive for workers to stay at work longer*. Note, we are not proposing changes to the age of rst receipt of GIS (currently 65). GIS should be available at age 65 because it is an important source of income for low-income earners.

4. Consider appropriate changes to other complementary programs such as provincial plans providing low-income seniors with additional income, such as Guaranteed Annual Income System (GAINS) or drug coverage.

5. Address any unintended consequences that deferring eligibility for retirement bene ts under CPP/QPP and OAS may have on low-income and disabled workers by considering measures such as decoupling the eligibility for GIS from the eligibility for OAS, and possibly increasing the $3,500 earnings exemption for contributions to the CPP/QPP. These measures would address concerns that low-income Canadians would not be treated fairly because of their lower life expectancy.

Chosen excerpts by Job Market Monitor. Read the whole story at Public Statement: Retire Later for Greater Benefits

Discussion

No comments yet.