Using two new datasets that link survey respondents from the 1991 and 2006 censuses of Canada to administrative tax records, this paper assesses the extent to which education affects how Canadians save and accumulate wealth for retirement.

First, using descriptive analysis, this study finds the following:

- Across groups of individuals based on their highest level of schooling attained—high school dropouts, terminal high school diploma or trades certificate, some postsecondary education, and university graduate—individuals with more schooling are more likely to contribute to a tax‑preferred savings account and to have higher savings rates in these accounts over the life cycle than those with less schooling.

- Similarly, home values at a given age increase with educational attainment, and the likelihood of renting housing decreases with educational attainment.

Second, this paper extends the descriptive analysis by estimating the causal effect of education on retirement savings rates, exploiting compulsory schooling reforms as an exogenous source of variation in education to identify this effect. This analysis shows the following:

- Controlling for demographics, income, health, and other channels through which education indirectly affects savings decisions, high school completion boosts retirement savings rates by 2 to 6 percentage points annually over the life cycle.

Third, education is shown to affect how individuals re‑optimize their savings rates in response to an automatic change in pension contributions to employer‑sponsored accounts. Specifically, the analysis builds on a recent study by Messacar (2015) and shows the following:

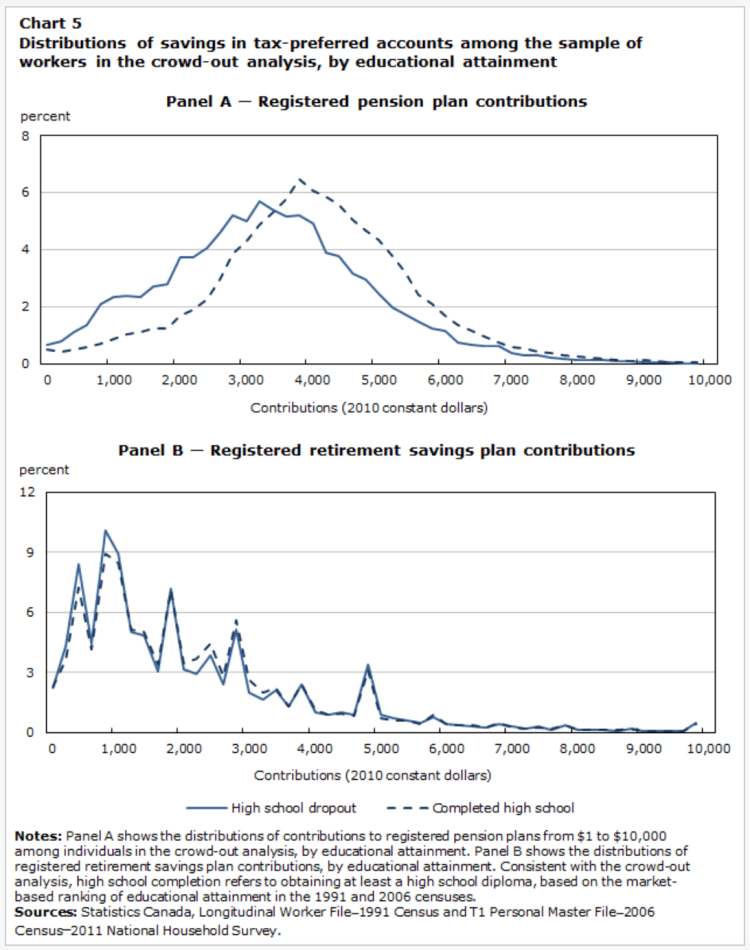

- Workers with lower levels of schooling are unresponsive to an automatic employer pension contribution. For this group, an exogenous increase in workplace pension contributions effectively increases total retirement savings.

- In contrast, workers with higher levels of education actively crowd out an automatic contribution by reducing how much they save in other retirement savings plans.

Taken together, these results indicate that individuals with lower levels of education save less for retirement than those with higher levels of education but benefit from an automatic contribution by remaining passive, whereas those with higher levels of education adjust savings across vehicles in response to an automatic contribution at low cost. The implications of this study’s findings for the “nudge paradigm” in behavioural economics are discussed.

via The Effects of Education on Canadians’ Retirement Savings Behaviour

Discussion

No comments yet.