State government pensions have attracted considerable media and scholarly attention. Less well understood are the nation’s 3,196 locally administered plans. The paper represents a first step toward filling this gap. After reviewing issues common to state and local plans, it summarizes existing data and research on local pensions.

Like many institutions now prevalent in state and local government, public employee pensions originated at the local level. New York was the first city to institute a plan for its police officers in 1857. Massachusetts followed suit with the first state plan in 1911.

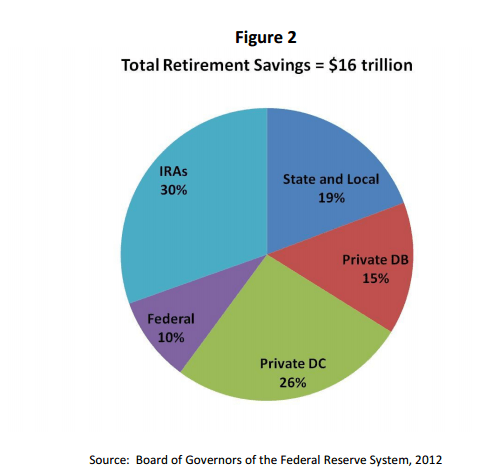

Today, state and local pensions are an important part of the nation’s retirement system. Every state has at least one public employee pension plan and Pennsylvania has 1,425 plans. As of the first quarter of 2012, state and local pension funds held $3.1 trillion in assets, or roughly one fifth of total U.S. retirement savings (Figure 2).

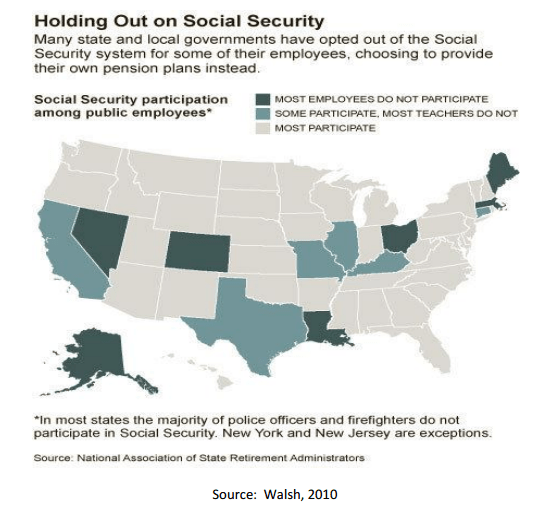

State and local pensions are all the more important because many government employees (roughly one quarter) do not participate in Social Security. This exclusion stems from historic concerns about the legality of a federal payroll tax on state and local governments. Starting in 1950, however, states could enter into voluntary “Section 218 agreements” to enroll their employees, and since 1991 all state and local workers not covered by their employer have been eligible for Social Security. The bulk of workers not covered by Social Security are teachers in California, Illinois, and Texas and general employees

in Alaska, Colorado, Massachusetts, Nevada, Ohio, Louisiana, and Maine (Figure 3).

Another key feature of state and local pensions is that they are typically defined benefit (DB) plans. Under these plans, benefits are calculated by formula, typically based on the product of final salary (often averaged over three to five years), years of service, and a credit (such as two percent) for each year of service. For example, an employee earning $50,000 in his final three years of employment after twenty years of service would be eligible for an annual pension of $20,000 ($50,000 multiplied by 20 and 0.02). As of 2009, DB plans covered nearly 80 percent of state and local workers, compared to 20 percent of private sector employees. Defined benefit plans used to be more prevalent in the private sector but have largely been

replaced by 401(k)-style Defined Contribution (DC) and hybrid plans. Explanations for this phenomenon include higher administrative costs and regulatory burdens for private DB plans since passage of the Employee Retirement Income Security Act of 1974 (ERISA) as well as less advantageous tax treatment since the Tax Reform Act of 1986 and subsequent legislation.

Local plans are as well funded as their statewide counterparts. However, applying a lower discount rate and generalizing from the nation’s largest municipal plans (those with assets above $1 billion), researchers have estimated aggregate unfunded liabilities of $574 billion. Results from an original news scan suggest that pensions are already burdening some local budgets. Key issues going forward will be determining how local government employee pension costs affect current municipal cash flows and whether pension funding status is capitalized in local property values.

Full Report @

via The State of Local Government Pensions: A Preliminary Inquiry (Working Paper)

Related Posts

US Public Pension Funding / Aggregate underfunding of $0.895 trillion

The Milliman Public Pension Funding Study independently measures the aggregate funded status of the 100 largest U.S. public pension plans using basic actuarial principles and reported plan liabilities and assets. The aggregate accrued liability information provided has been determined on a uniform basis with respect to the interest rate assumption across all of the plans … Continue reading »

Pension Plan / Less than a third of Fortune 100 Companies offer a defined benefit plan to newly hired salaried workers

In 2012, the number of Fortune 100 companies offering new salaried employees only a defined contribution (DC) plan rose, as it has for many years. Today, less than a third of these companies offer any DB plan to newly hired salaried workers, and only 11 still offer a traditional DB plan to new hires. Large … Continue reading »

US – Study shows $1.2 trillion gap for public pensions

The largest 100 public pension funds have around $1.2 trillion of unfunded liabilities, about $300 billion above the nearly $900 billion they reported themselves, according to a new actuarial study to be released on Monday. The pension systems reported a median funding level of 75.1 percent. The study by the actuarial firm Milliman, which used … Continue reading »

Pensions after the financial and economic crisis: a comparative analysis of recent reforms in Europe

”This paper look at the impact of the economic and financial crisis on pensions policy across Europe, and assesses the first measures proposed and/or introduced in four EU countries. France and Sweden are typical examples of social insurance systems, while Poland and the UK are examples of multipillar systems.” writes David Natali in Pensions after the financial and economic crisis: … Continue reading »

I blog quite often and I really appreciate your information.

The article has truly peaked my interest.

I’m going to bookmark your blog and keep checking for new information about once a week. I subscribed to your Feed too.

Posted by password generator | April 13, 2013, 12:31 amamazing insight. Really enjoyed reading this blog. Keep up the good work and to everyone keep on learning!

Posted by www.clubespresso.co.kr | September 4, 2014, 1:38 am