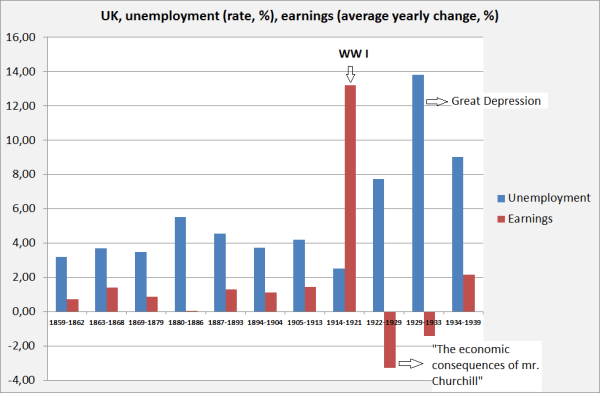

‘New-Keynesian’ models use sticky prices and downward rigidity of nominal wages to get ‘Keynesian’ results: during slumps, low interest rates, money growth and additional expenditure (not necessarily government expenditure) can heal the economy and lower unemployment without inflationary consequences. The name ‘New-Keynesian’ is however a double travesty. Not because prices aren’t sticky (many are) or because downward rigidity of nominal wages does not exist (it exists). But because in the ‘General Theory’ Keynes argued that slumps can happen despite and even because of declining wage income and downward flexible wages. And because he had good reasons to do this: after 1921 english wages showed an unprecedented long-term decline while unemployment stayed way above historical levels and increased to unprecedented levels after 1929. An implication of (almost all) ‘New Keynesian’ models is that economies will bounce back to full employment if only labour and other markets are ‘flexible’ enough. The UK example shows that this isn’t necessarily the case. Keynes explained why. New Keynesian models don’t. As far as I’m concerned, data like those below should be part of any undergraduate introduction into Keynesian economics.

Chosen excerpts by Job Market Monitor. Read the whole story at Understanding Keynes: the data | Real-World Economics Review Blog.

Related articles

- Listen to John Maynard Keynes’ voice on High Unemployment

- Krugman – Macro 101 – Sticky Wages

- John Maynard Keynes shows us a way out crisis

- Mass Involontary Unemployment

- Unemployment – Hurts more than just the Unemployed

- US / Long-term unemployment has less impact on the behavior of wages study says

- US / Wage stickiness might be dying out

Discussion

No comments yet.