The house and equity price busts on top of a credit crunch make this an unprecedented crisis for the modern US economy; its real economy effects are thus difficult to assess. This column provides insights based on evidence from 122 recessions in 21 advanced nations since 1960. Findings suggest recessions in such circumstances are much costlier and slightly longer. But the outcome can be affected by policy, and it’s high time that policymakers act swiftly and decisively.

How costly are recessions?

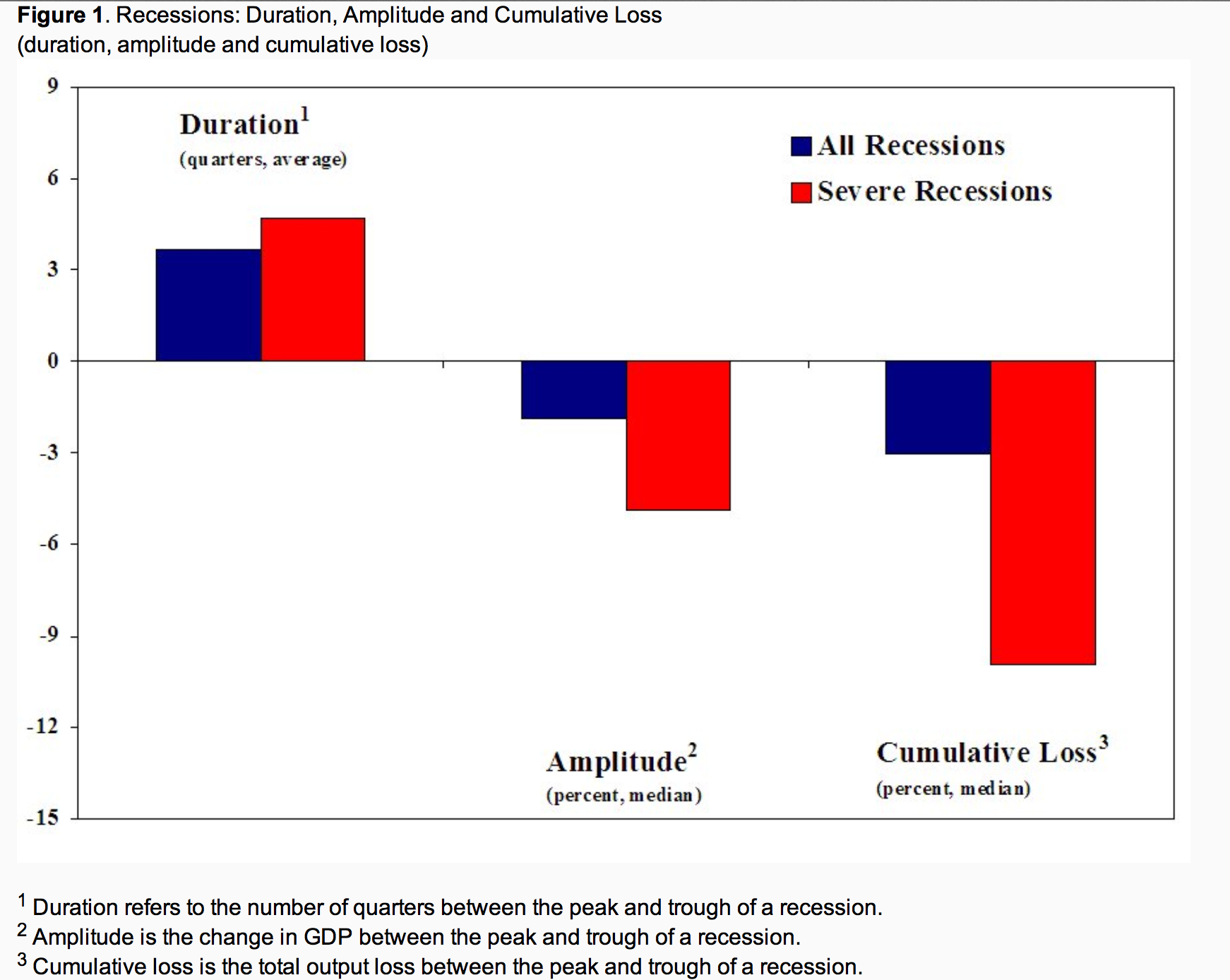

As shown in Figure 1, a recession on average lasts about 4 quarters (one year) with substantial variation across episodes — the shortest recession is 2 quarters and the longest 13 quarters. The typical decline in output from peak to trough, the recession’s amplitude, tends to be about 2 percent. For recessions, we also compute a measure of cumulative loss which combines information about both the duration and amplitude to proxy the overall cost of a recession. The cumulative loss of a recession is typically about 3 percent of GDP, but this number varies quite a bit across episodes. We classify a recession as a severe one when the peak-to-trough decline in output is in the top-quartile of all output declines during recessions. These recessions tend to be more than a quarter longer and much more costly than do typical recessions.

Crunches and busts: Often long and painful

The episodes of credit crunches and housing busts are often long and deep (Figure 2). For example, a credit crunch episode typically lasts two and a half years and is associated with nearly a 20 percent decline in real credit. A housing bust tends to last even longer: four and a half years with a 30 percent fall in real house prices. And an equity price bust lasts some 10 quarters and when it is over, the real value of equities has dropped to half.

Chosen excerpts by Job Market Monitor. Read the whole story at

![]()

via Five decades of evidence on financial crisis and recession: How long? How deep? | vox.

Discussion

No comments yet.