Following a recovery from the middle of 2009, the EU economy and manufacturing industries retreated into a double-dip recession since the end of 2011 (Figure 4). Employment in manufacturing has been steadily declining for decades and this decline accelerated with the outbreak of the financial crisis. As a result, the share of manufacturing in GDP continued shrinking from 15.8 % before the crisis to 15.1 % in 2013. But the share of manufacturing has long-term structural explanations as well. For instance, manufactured goods can be traded more easily and produced increasingly more efficiently than other outputs. Against that backdrop and in combination with rising incomes, the relative price of manufactured goods is likely to fall in relation to the price of services. Thus the weight of the services sectors in the GDP has been increasing, while the weight of manufacturing has been falling.

Figure 4. Double-dip of EU manufacturing production

Source: Own calculations using Eurostat data

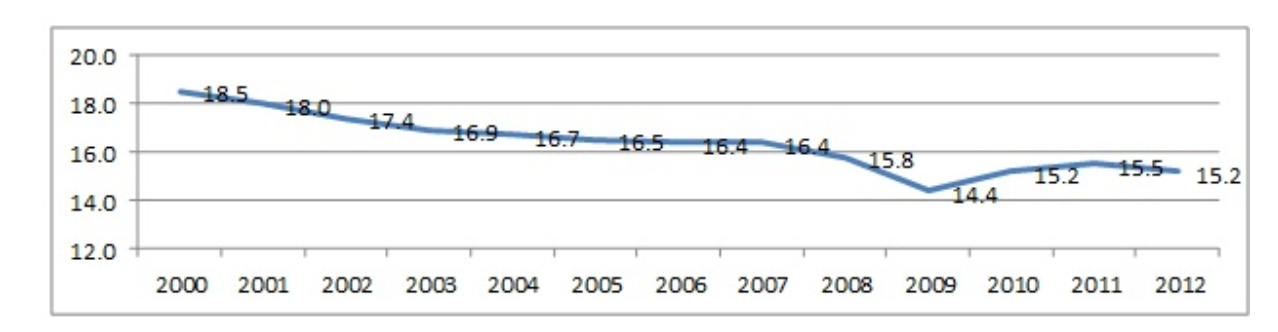

Figure 5A. Declining share of manufacturing in EU GDP

Figure 5B. Changes in the share of manufacturing in the EU MS 2000-2012

Source: Own calculations using Eurostat data.

In spite of longer-term trends in advanced economies of the manufacturing sector accounting for a shrinking share in value added and in employment, there is a strong case for preserving a ‘critical size’ of manufacturing activities in European economies. There are very important ‘backward linkages’ from manufacturing to services which provide important inputs for manufacturing (in particular business services). Thus, manufacturing has a ‘carrier function’ for services which might otherwise be considered to have limited commercial value. In the same direction goes the increased ‘product bundling’ of production and service activities in advanced manufacturing activities. This ‘carrier function’ – through international competitive pressure – has furthermore a stimulus effect for innovation and qualitative upgrading for service activities. Because of this increasing cross-over (Figure 6), when manufacturing is struggling this has a very negative impact on services sector and on the overall economy and jobs.

Figure 6. Increasing share of services in manufacturing sectors

Source: World Input-Output Database

Chosen excerpts by Job Market Monitor. Read the whole story at

Discussion

No comments yet.